Auto Partner SA

Spare part distributor with 25% average ROE trading at a forward P/E of 9x.

Auto Partner SA is one of the largest distributors of automotive parts in Poland, with PLN4bn in revenue, 2,700 employees, and a ca 10% market share. The Company has ca 280k product references from over 350 suppliers available, and also has private label brands, including maXgear, which represent around 20% of revenue. These products are stored in ca 160,000m2 of warehouse space, in warehouse facilities of varying sizes, complemented with logistics and distribution centers and branch offices. About 70% of orders are placed online, and the Company operates a just-in-time delivery model, enabling deliveries with a frequency of 3-5 times a day. In Poland, customers consist of repair workshops (62%), specialised stores (30%), and non-specialised repairers and retailers (8%). The Company also uses its low-cost base and efficient logistics network to supply neighboring countries, which account for around 50% of group revenue.

Auto Partner’s main competitors are Inter Cars (ca 30% market share in Poland), Inter Team (9-10%) and H.M. Gordon (ca 7%), with the rest consisting mostly of smaller, more fragmented competitors.

Financial Overview

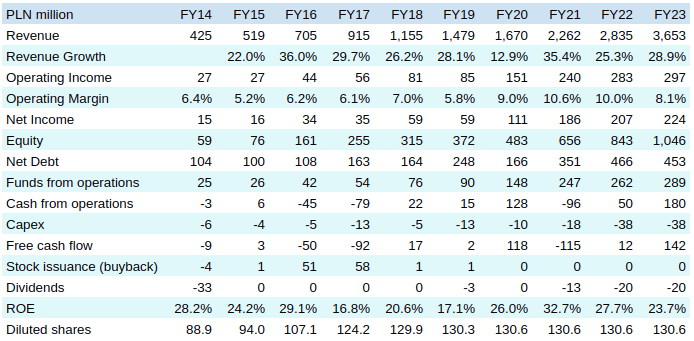

The Company’s track record over the past decade has been impressive, with revenue increasing by over 8x, and the operating margin increasing at the same time, resulting in a ca 10x increase in operating income and 15x increase in net income. There was some dilution over that period as the Company had to issue some equity to fund part of that growth, but the EPS increased by a still impressive ca 9x. Also interestingly, all of that growth has been organic; there has been no M&A and the Company has no goodwill.

The Company’s business model is relatively simple. Customers want a one-stop shop that can provide all the parts that they need, rather than having to order them from dozens or hundreds of different suppliers. And they want these parts for the best possible price, and as fast as possible. So to take market share, Auto Partner needs to increase the density of its distribution network (for faster delivery); increase the amount of product references in stock; and expand geographically, in Poland or overseas. In turn, this means that growth will take place mostly through increases in capex (warehouses, trucks etc) and inventory, hence the large increase in working capital needs and capex over the past decade. Notwithstanding these large investments, high asset utilization has led to a more than satisfactory return on equity, at ca 25% on average.

The Company has started to pay a small dividend in FY21 although regrettably no share repurchases so far; a common shortcoming in European companies, even though they generally trade at much lower valuations than in the US, where it’s much more common Why it is so hard for management teams to repurchase shares when it’s accretive is beyond me.

While margins have trended higher over time due to increased scale and network effects, we can also notice that there was a sudden jump in operating margins during the covid period (FY20-FY22), driven by a shortage of car parts and strong demand, with margins normalizing starting in FY23.

Auto Partner has released preliminary results for FY24: 12.6% revenue growth to PLN4.1bn and PLN285m in operating profit, resulting in an operating margin of 6.9%. That corresponded to the lowest annual revenue growth of the past decade, and the weakest operating margin since FY17. The Company was impacted by two main items: (i) relatively weak PLN exchange rates, increasing the cost of goods sold; and (ii) higher staff costs, with notably a 21.5% increase in Polish minimum wages in January 2024.

Management & Ownership

The Company was founded in 1993 by Aleksander Gorecki. He still runs the company and has a 43.6% ownership stake (same voting share). That’s the textbook example of what I like to see - a company led by an entrepreneur with a growth mindset, who still owns a significant stake in the business. And I haven’t come across anything that would lead me to believe he’s taking advantage of minority shareholders, it all looks fairly clean. There are some related party transactions, including purchases of services from entities related to members of the management board amounting to PLN2.9m, quite negligible compared to net income or equity. Management remuneration does not seem shocking given company size. And the Group has made a loan of PLN27.2m to the CEO and his wife - not great, but not material either, I’ve definitely seen worse.

Prospects & Valuation

The Company currently trades at a forward P/E of 9x, which sounds fairly reasonable given the track record, and a forward EV/EBITDA of 8x, which is roughly where it has historically traded. The trailing P/E is at ca 13x, and the trailing EV/EBITDA at ca 11x - that’s uncomfortably high compared to the other stocks I’ve written about so far on this blog, which usually trade at half that valuation.

Here my thesis is straightforward - in my view the company’s business model is as strong as it’s ever been. Margins have partly returned to the mean following abnormally high margins during covid, and were then further impacted by temporary factors - FX rates, and an increase in the Polish minimum wage to catch up with covid-era inflation. Auto Partner has higher margins than Inter Cars, the largest operator on the market, and I suspect its margins are higher than that of its other competitors as well. If FX rates and increases in Polish minimum wages are pressuring Auto Partner, I can only imagine the situation for smaller operators that do not have the same scale. That should lead to further consolidation in the industry, and over time to higher margins for Auto Partner. If the Company continues to grow revenue at a solid pace while its operating margins recover, that should lead to satisfactory results. The level at which margins stabilize is anyone’s guess, but for what it’s worth, the analysts covering the company assume the trough was in FY24 and that margins will bounce back from here. The minimum wage in Poland was increased by 8.5% in January 2025; still high but better than the ca 20% from the previous year.

And over the longer term, there are both clear headwinds and tailwinds. As Auto Partner is an efficient operator with a relatively low market share, it should be able to grow by taking market share in a fragmented industry. On the other hand, the EU has banned new petrol and diesel cards from 2035, and all cars on the road will have to be EVs by 2050; this would be a threat to Auto Partner as electric cars have much less car parts than combustion engine cars. This is a complicated issue - in my view, the transition to EVs will take much longer, and current timelines are not realistic. There is already talk about revising this ban. And China currently has a lead in EV production; I can’t imagine the EU deciding to in effect just close its own car industry, lay off the whole EU auto workforce, and give its car market to China. So in a worst case scenario, Auto Partner has another 25 years of runway, with a full transition to EVs then potentially having an impact, although there could be delays to this transition and/or the transition to EVs may not have as material an impact as feared. In any event, that’s why it’s always best to buy companies at low valuations.

Conclusion

Auto Partner has an excellent track record driven by network effects, with economies of scale and increasing network density. While it only has a market share of ca 10%, it is better run that its larger peer Inter Cars, which has lower margins and a lower ROE. This should translate for Auto Partner into a long growth runway, with the Company further increasing its market share over time and making it more and more difficult for its peers to compete.

If your portfolio is already full of companies that can 10x EPS over 10 years with a long runway ahead of them while trading at a single digit forward P/E multiple then Auto Partner will probably be of no interest to you. Otherwise you should consider looking into this company…

Links

I have to say that for a relatively small Polish company, I’m quite impressed by the quality of the financial disclosure. The company prepares high quality financials and investor presentations in English, readily available on its website.

Some investors have written about Auto Partner SA in the past, I’ve found a few articles through Twitter. The most interesting article I’ve come across is probably the one from Sohra Peak’s Jon Cukierwar, here is a link to his 2022 write-up. While it was written three years ago, I don’t think there’s been any fundamental change to the thesis since then - his main issue was timing as he wrote about the company at a point in time when Auto Partner’s margins were abnormally high (only obvious in hindsight, and even so the share price has gone up nicely since then, notwithstanding a steep decline in 2024):

https://mcusercontent.com/3fff1ea9d792aab7f6dffe0ab/files/ccc97c91-fc8f-09c6-53f2-0e9109d1cb71/Auto_Partner_SA_Condensed_Thesis_August_2022.pdf