Build King Holding

16% ROE Business Trading at Negative EV

Build King is a Hong Kong-based construction and civil engineering group with HKD13.8bn in revenue, ca 3,600 employees, and an order book of HKD30.8bn. The Company holds a Group C license, allowing it to tender for public works contracts of unlimited value - this provides a moat as it prevents smaller contractors from competing. The company’s operations are divided into three primary segments:

(1) Civil Engineering (HKD8bn revenue, HKD508m gross profit). Their bread and butter, covering complex infrastructure like tunnels, bridges, and maritime works. Key active projects include the central Kowloon route (that’s the picture I used for this article - the elevated, curving flyovers highlight the quality and complexity of the projects that Build King works on); the Tung Chung new town extension (significant reclamation and site formation work); and the relocation of the Sha Tin sewage treatment works (large-scale cavern construction).

(2) Building Construction (HKD5.1bn revenue, HKD305m gross profit): Residential and commercial building projects, often for the public sector. Projects in backlog are for the Hong Kong Housing Authority and the Architectural Services Department.

(3) Environmental & Energy (HKD1.4bn revenue, HKD186m gross profit): A growing niche involving sewage treatment and steam fuel plants in Mainland China, providing a small but steady diversification away from pure construction.

Financial Overview

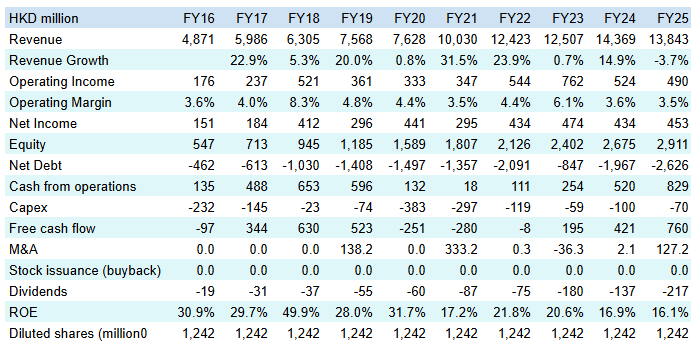

As would be expected from a construction company, revenue growth and margins are not smooth as they depend on timing of project completions. That being said, the overall revenue CAGR over the past decade amounted to over 12%, which is quite impressive and probably not what people expect from a construction company. To note - there was a revenue decline in 2025 resulting from delays on new contracts, with the Company unable to commence construction work due to land resumption issues. The operating margins are relatively low, typically at 3-4%, reflecting the tender-based nature of the industry, where volume is the primary driver of profit. Nevertheless, net income has tripled over that period. This growth was entirely self-funded, with no share price dilution, no meaningful acquisitions, and with increasing shareholder returns, as the dividend increased by more than 10x, growing at a much faster pace than net income. And this was all done in a very prudent manner, with the Company holding a net cash position throughout the whole period.

Management & Ownership

Derek Zen, Chairman and CEO, age 73, has over 40 years of experience in the industry. With his brother William Zen, he founded the Wai Kee group in 1980. Build King was listed in 2004 to hold the construction interests of the Wai Kee group, with Derek Zen serving as chairman of Build King since its listing, providing stable stewardship. The Wai Kee group still owns 58% of Build King. Derek Zen has been a consistent and active buyer of Build King shares, directly owning a further 9.9%. His latest purchase took place on the 20th of October 2025 - 2.5m shares amounting to HKD3m. Importantly, these are not stock grants but open market purchases - as noted above, there was no dilution.

Prospects & Valuation

Due to the HKD30.8bn order book, there is already visibility on over two years of revenue. Further out, the outlook for Build King is tied to the Hong Kong Government’s “Northern Metropolis” and “Lantau Tomorrow Vision” initiatives. These multi-decade infrastructure projects ensure a massive pipeline of civil engineering work. The government announced an increase in spending on infrastructure from HKD120bn to HKD150bn per annum in 2026 - Build King would need to win ca 10% of that envelope to refresh its backlog. While private sector construction can be cyclical, Build King’s heavy exposure to essential public infrastructure provides a defensive floor. Revenue and earnings are likely to trend upward simply due to the sheer volume of mandated infrastructure spending in their home market.

With a current market cap of ca HKD2.3bn and a net cash position of HKD2.6bn, Build King has a negative enterprise value. Usually, companies with negative EV are value traps, with low ROE and low or no shareholder returns. Here, the business has an ROE of 16%, and the forward dividend yield is ca 9.5%. So if you buy Build King shares, you get a cash account with a rebate; a 16% ROE business thrown in for free; and the cash is actually being returned to shareholders at a solid pace.

In terms of potential risks, the main ones I can see are as follows: (i) inflation. Most of the company’s public works contracts include price adjustment clauses. Price increases, including for the price of fuel, are automatically passed on. (ii) Shifts in government fiscal policy. The budget is effectively locked for the next five years, although some tenders could be delayed. And in 2026, the government increased infrastructure spending by HKD30bn, so for now it is a tailwind. (iii) Competition. While the order book is robust, the entry of large mainland SOEs into the HK market is putting downward pressure on margins. Derek Zen has countered this by being selective, resulting in an ROE that, while trending down, remains healthy at 16%. (iv) End of the USD/HKD peg. This is a low probability event but still worth mentioning. If it were to materialise, it could lead to a depreciation of the HKD of perhaps up to 30%. For now it’s mostly hypothetical and not on the cards.

One last point - as a Hong Kong small cap, the daily liquidity of the shares is low, at around USD100k per day. While it’s more than sufficient for an individual investor to build a position, it’s well under the threshold of institutional funds. This is also what creates the mispricing.

Conclusion

Build King is a solid defensive investment. While there is no catalyst guaranteeing a quick share price re-rating, this is a solid company with high ROE, a backlog covering over two years of revenue, and a negative enterprise value. With a dividend yield of nearly 10% and a CEO consistently buying shares on the open market, investors are effectively being paid to wait.

Build King currently represents 5% of my portfolio. With its negative EV, it’s mathematically the cheapest stock I own, offering a good margin of safety.

How did you calculate net cash? I.e., did you include any liabilities resulting from received prepayments?