Greens Co Ltd

An asset-light, high-ROE Japanese hotel operator trading at 6x P/E.

Greens Co is a Japanese hotel operator. It operates 102 hotels, split between two segments: (i) Choice Hotels (75% of revenue, 13.9% EBIT margin). The Company is the exclusive master franchisor for Choice Hotels International in Japan. The bulk of the portfolio (ca 70 properties) consists of Comfort Hotels - limited service hotels located near major railway stations, targeted at inbound tourists and domestic business travelers with efficiency in mind; (ii) Greens Hotels (25% of revenue, 9% EBIT margin). Destination hotels with a full-service concept, targeting the local community (banquet halls, wedding facilities) and local tourism. The margin is lower due to the full-service features, which are more labour intensive.

Approximately 50% of revenue corresponds to domestic business travelers, providing stable revenue including during the off-peak tourism months. Another 15-20% corresponds to domestic leisure, filling weekend gaps and regional properties. And the balance, 30-35%, corresponds to international travelers, particularly from North America and Europe. These travelers tend to be higher-margin, being less price-sensitive than domestic business travelers, and staying on average for longer, thereby reducing the operational turnover costs associated with single-night business stays.

Financial Overview

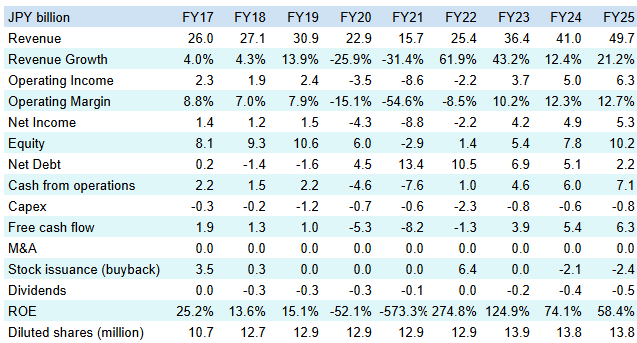

The Company went public in 2017. Back then, revenue was split ca 50/50 between the two segments, and management used the IPO proceeds to scale the higher-margin Choice Hotels business. Revenue has grown at a good pace since then (ca 7% CAGR), and the operating margin expanded over time from 8.8% to 12.7% due to the shift towards the higher-margin Choice Hotels business. Increased business size has also led to economies of scale, with centralised procurement; optimised staffing, with mobile staff units that can move between properties in the same city based on occupancy surges; and booking data from over 15,000 rooms to feed an AI-driven dynamic pricing engine.

Greens Co was unsurprisingly impacted by COVID, sustaining heavy losses in 2020 and 2021. As the Company has an asset-light model (also visible at low capex) and does not own the underlying real estate, it had to keep making rent payments through the downturn, and was forced to issue shares to survive, explaining the increased share count.

The Company then had a solid recovery over the following years. The Company’s financial debt should soon approach zero, although as mentioned above, as it operates nearly all its hotels via lease agreements, it also has ca JPY58.4bn in leases, which are not included in the above net debt numbers. And the Company started repurchasing shares over the last two years, although unfortunately so far the repurchased shares were not cancelled but kept in treasury or used for employee grants. Management is now evaluating the cancellation of 2% of outstanding shares held in treasury as a potential “first tranche” - my guess is that this will happen once the company is debt-free, if no significant headwinds materialise, so potentially within six months. And while it’s not visible in the above table, management has also increased capex to upgrade its hotels, for renovation but also to increase technology and automation (such as self check-ins), which should enable the Company to increase average day rates.

Management & Ownership

The CEO is Takeya Muraki. He is the son of the founder, joined the Company in 1997 and became CEO in 2018. He led the Company through COVID, and the recent digital transformation initiatives, including dynamic pricing and automated check-ins. He directly owns ca 8.2% of Greens Co, providing alignment with shareholders. Other key shareholders include the wider founding Muraki family, which own ca 40% of the voting rights through a number of holdings. And the Regional Economy Vitalization Corporation of Japan owns a 7.2% stake since the 2022 share issuance.

Prospects & Valuation

The Japanese government aims to increase inbound visitors from 42.7 million in 2025 to 60 million in 2030, with total spending increasing from JPY9.5tn to JPY15tn. This growth will rely on markets outside of the Golden Triangle of Tokyo-Osaka-Kyoto. Greens Co is well positioned for this, due to its significant footprint in regional cities.

Management also has ambitious targets, and aims for JPY80bn in revenue by 2030, compared to ca JPY50bn currently; and ca JPY10bn in operating profit, compared to ca JPY6.3bn currently. To get there, management wants to (i) operate ca 150 hotels, thereby further increasing economies of scale; (ii) shift the portfolio towards a more premium mix, to increase Average Daily Rates; and (iii) increase direct bookings, thereby reducing commission fees paid to online travel agencies like Expedia or Booking.com. Given the company’s track record over the past decade, these targets do not seem unrealistic - in typical Japanese style, management tends to provide conservative guidance and then over-deliver during normal times.

The Company is currently valued at a trailing P/E of ca 6x, and a lease-adjusted EV/EBITDA of ca 6x. These are multiples typically reserved for contracting businesses, whereas Greens Co is demonstrably in an expansion phase. Peers trade at lease-adjusted EV/EBITDA multiples in the 10-13x range, although admittedly these peers are larger. Looking at historical valuation multiples, prior to COVID, Greens Co traded in the 8-10x range, with its asset-light expansion model valued more generously. The bull case for this stock would be management hitting the JPY10bn EBIT target by 2030 and the EV/EBITDA multiple going back to 10x, which could lead to a 4x increase in the share price.

Regarding downside, here are a list of potential risks: (i) Geopolitical developments. In the shorter term, there should be a dip in 2026, largely driven by a cooling of the Chinese market following diplomatic tensions. Chinese travelers represented ca 20% of inbound visitors to Japan, and their numbers have dropped precipitously, which led to a 4.9% year-on-year drop in tourism in Japan in January. Management has reallocated marketing spend toward North American and European markets to replace Chinese travelers, which are estimated to represent 6-8% of group revenue. Further negative geopolitical developments could have an adverse effect on the Company. As a mitigant, Greens Co’s large base of domestic business travelers should help cushion any impact to the downside. (ii) Labour shortages. In Japan, there is also acute labor shortage, although so far Greens Co as been able to navigate that successfully through digital transformation. (iii) Master franchise agreement. Greens holds the exclusive rights for Choice Hotels in Japan since 2003. The master franchise agreement was extended for 10 years in 2019. And as long as the Company meets its growth milestones, renewal should be a formality. (iv) Currency appreciation. It would make Japan less of a “value” destination. Foreign investors have a natural hedge here - if the currency appreciates then so will the share price.

Conclusion

Greens Co is a hotel operator with a solid track record and ambitious growth targets. In a bull case, the share price could quadruple over the coming four years. Even if there are headwinds, performance should be adequate given the starting valuation. However clearly the company is also cyclical and levered due to the leases, as became evident during the COVID crisis. Based on the above, I see this company as a good bet as part of a wider diversified portfolio, and I’ve made a small investment in that company. Over the coming year the two main items to watch will be the impact of Chinese travelers on Greens, and the potential treasury share cancellation. If the impact from Chinese travelers is muted / offset by more Western travelers and treasury shares cancelled, we could potentially see a meaningful share price move. And in case of adverse news, the very low starting valuation should act as a cushion.