Renold PLC

Industrial machinery company trading at 4.5x P/E.

Founded in 1864, Renold is an international engineering group specializing in the manufacture of premium, high specification, industrial chain and torque transmission products, with £240m in revenue and ca $40m in adjusted EBITDA. The Company is based in the UK and operates in two segments: (i) industrial chains (ca 80% of revenue, ca 17% operating margin) and (ii) torque transmission products (ca 20% of revenue, ca 16% operating margin).

Management estimates that the total size of the global Chain market is over £3bn, with Renold being global #2 with around 7% market share in an extremely fragmented sector. The Company’s products are very niche, even within this £3bn market, with a focus on the higher end. These products are mission-critical, but are only a small part of the total cost for the client. The higher cost of premium chains is insignificant compared to the cost of downtime if a lower quality chain fails. And approximately 75% of sales are for repair and maintenance - in other words, a high proportion of revenue is recurring.

Renold serves every conceivable industry, with the main ones being Manufactured Products (27%), Material Handling (9%), Transportation (9%), and Mining & Quarrying (9%). In essence, anything that moves needs industrial chains: escalators and elevators; conveyor belts for food processing; manufacturing and packaging; warehouse automation; forklifts; bulk material handling; recycling; dams; theme parks, etc. There are thousands of applications for industrial chains. There is no concentration risk, with Renold’s largest client accounting for ca 3% of revenue.

The above picture is useful to better understand what Renold does. The company’s focus is on tooth chain, transmission chain, conveyor chain and leaf chain. Renold does not manufacture bicycle chain, motorcycle chain or automotive chain. And management sees table top chain and bi-planar chain as expansion opportunities.

Geographically, the Company has manufacturing capacity in Europe (primarily Germany and Spain), in the US and in Asia Pacific (Australia, Malaysia, India and China). Revenue by end-market is split between the Americas (42% of revenue), Europe (39%), Asia Pacific (10% - corresponds to Australia, Malaysia, New Zealand, Indonesia and Thailand) and High Growth Economies (9% - corresponds to China and India).

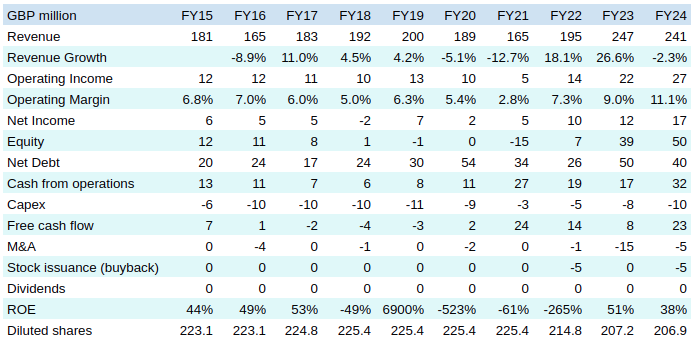

Financial Overview

This company reminds me of McBride. It’s been through a rough patch, with low margins and uneven profitability. Over the past decade, the company closed its production facilities in the UK, opened a new factory in China, went through a widespread re-engineering of business processes and upgraded its IT systems. This resulted in a marked improvement in operating margins, which increased from mid-single digits to double digits. The restructurings ended in FY20 although that is not immediately apparent as the Company was then impacted by covid, in FY20 and FY21, resulting in temporarily lower volumes and margin pressure. And with the restructurings complete, the higher cash flow generation capacity allowed Renold to start making bolt-on acquisitions: (i) Industrias YUK S.A., acquired in FY23. It is a Spanish manufacturer of conveyor chain which added £18m to revenue and was acquired for ca £17m; (ii) Davidson Chain, acquired in FY24. It is an Australian manufacturer and distributor of high-quality conveyor chain and adapted transmission chain with ca $1.6m in revenue, acquired for £3.1m; and (iii) Mac Chain, acquired in FY25 (the company’s financial year-end is in March). This company is a manufacturer of conveyor and transmission chain based in Canada and the US, has ca $25.8m in revenue, and was acquired for ca £23.8m, or 7.5x EBITDA (management aims to take that to 6x EBITDA or lower through the realization of synergies).

Further showing that the Company turned a corner, we can see that it made share repurchases in FY22 and FY24. And in the current year (FY25), Renold also reintroduced a dividend amounting to £1m - that was the company’s first dividend in 19 years.

I mentioned at the start of this write-up that Renold was founded in 1864 - that shows that its products have been in use for a long time. There is a drawback to old companies though - they tend to have unfunded pension liabilities, from back when providing defined benefits was the norm. Renold is no exception, and has £52.2m in unfunded pension liabilities.

And I usually like to use return on equity to assess companies. Here it’s difficult: for a long time Renold had a thin equity base or even negative equity. Nevertheless, over the last couple of years the Company rebuilt its equity base with ROE becoming more meaningful, and the ROE was solid, largely above 20%. If we look at alternative metrics such as return on assets or EBIT/assets, the performance has been satisfactory as well over the last couple of years.

Management & Ownership

I prefer companies to be founder-led, however as Renold was founded in 1864, clearly that wasn’t going to happen. The stock is widely-held, mostly by investment management companies. The CEO, Robert Purcell, 62, was appointed in 2013; he’s therefore overseen the whole successful turnaround, and he owns 2.5% of the company. The chairman, David Landless, joined the board in 2017 and was appointed chairman in 2021.

Prospects & Valuation

I would expect Renold to grow revenue organically at low single digits going forward, if only to reflect inflation, assuming constant volumes. And in line with management strategy, there should be further growth from M&A. If we do believe that an industrial renaissance will take place in the US and Europe, with re-shoring as well as large spend on infrastructure and rearmament, given that industrial chains are used everywhere, surely Renold should see some benefit as well, which could lead to higher growth rates. The Company has continued its upward trajectory in operating margins in 1H25 and that is expected to continue going forward, notably through M&A, with central costs remaining fixed while in particular the industrial chain segment keeps growing. Based on the above, I would expect the Company to continue to generate an underlying ROE higher than 20%.

The company currently trades at an undemanding 4.5x trailing P/E. Forward P/Es are somewhat skewed as YUK’s business in Spain was impacted by recent floods, resulting in ca £10m in damages, which should however mostly be recovered through insurance; this will lead to a ca £10m extraordinary cost followed in FY26 by a similar extraordinary gain (the net cost is expected to amount to ca £1m). As a result, the FY25 P/E is estimated at 6x, with the FY26 P/E at 3.5x, followed by a normalization in FY27 at 4.4x.

If we look at EV/EBIT, following the acquisition of Mac Chain, Renold has £42m in net debt. Current market cap is £87m, and we also have to add back the £52.2m unfunded pension liabilities. That adds up to £181m; compared to £27.1m in trailing EBIT, that results in an EV/EBIT of 6.7x. There are cheaper companies out there, but not many. And if we use EV/EBITDA instead, we get a multiple of ca 4x, including the unfunded pension liabilities. Notably, it’s interesting to see that the Mac Chain acquisition was done at 7.5x EBITDA; the Renold share price would need to go up ca 150% for the company to be valued at a similar EV/EBITDA multiple, as a majority of the EV consists of debt. Whichever way we look at it, Renold is cheap.

There’s been some weakness in the Renold share price recently, with a ca 30% decline over the past six months, and with most of the decline taking place since early February. There’s no apparent reason for this - I couldn’t find any recent news; broker price targets and earnings estimates have remained unchanged; and I haven’t seen any discussion of that company on social networks over the last two years. Regarding tariffs - about half of US revenue is manufactured locally, with the other half being mostly from Europe, and only a small percentage coming from China, amounting to ca £2m/year, according to management. There isn’t sufficient production capacity in the country to replace that, and as these products have a very small cost to clients relative to cost of downtime, customers just pay up for the industrial chains from China. Management also mentioned having flexibility to relocate production, if necessary, so I would expect tariffs to have a very limited impact. And if anything, European rearmament should be a tailwind. So perhaps Renold was impacted by some other event that I missed, or the share price is just going down due to complete lack of investor interest.

Conclusion

Like McBride, Renold has gone through a successful restructuring and is now in much better shape, with double-digit operating margins as well as solid cash flow generation which is used for M&A as well as shareholder returns. So the turnaround already happened and was successful; we can now see the new margins. But somehow, Renold is still valued like a distressed company. I’ve made a small investment in that company and would have made a larger one if it weren’t for the unfunded pension liabilities. I could still further increase my position if Renold continues to perform well while the share price remains reasonable.

I think what's really holding the valuation back is that unfunded pension liability. Sure the £52m feels precise, but its just based off of actuarial reports and their assumptions, change the assumptions, change the liability.

That was my take when I looked at Renold, there's a few other very small microcap UK companies with these legacy unfunded / underfunded defined benefit pension plans which just shift all the risk onto the employer and not the employee, imagine thinking of taking this over and trying to cap that liability, that's where I reckon the discount is coming from.