Tarczynski S.A.

Polish meat producer with 33% ROE trading at 9x P/E.

Tarczynski is an innovative Polish producer of meat products, with ca PLN2bn in revenue (ca €450m). The Company offers a range of ca 300 meat and sausage products, and is notably the leader in the pre-packed kabanos category in the premium segment, with a market share of >70%. Kabanos are traditional Polish sausages that are thin, dry and can be eaten as a snack or appetizer. The Company was founded in 1989 and has grown rapidly since then, with a focus on strong branding and premium products. Its conveniently packaged products are sold in the snack aisle as opposed to the meat counter, and are at higher price points than competition, but still affordable. The Company’s innovation is not just in the branding and packaging but also in the product offering, with a large range of products, including plant-based alternatives, and a diverse range of flavors, with options like cheese, chili, jalapeno, and piri-piri. The Company’s aim is to become the leading Polish producer of durable cold cuts, as well as the market leader in the meat snacks segment. While the Company’s revenue is still generated predominantly in Poland, as at 1H24 ca 30% of its revenue came from abroad (mainly Germany, the UK, Ireland and Sweden).

The Company produces its cold cuts at two plants in Poland. It does not have in-house breeding or slaughter facilities. About 60-65% of operating costs are raw materials, mostly pork but also other meats such as beef, chicken and turkey, with other raw materials including packaging (paper, film), spices and other ingredients. Margins can be impacted by fluctuations notably in pork prices. The drivers for pork prices include health issues affecting livestock such as the African Swine Fever; feed costs (grains and oilseeds); consumer demand (shift towards poultry); and international trade (China is a major export market which has recently seen reduced demand, and there is also competition from the US and Brazil).

Financial Overview

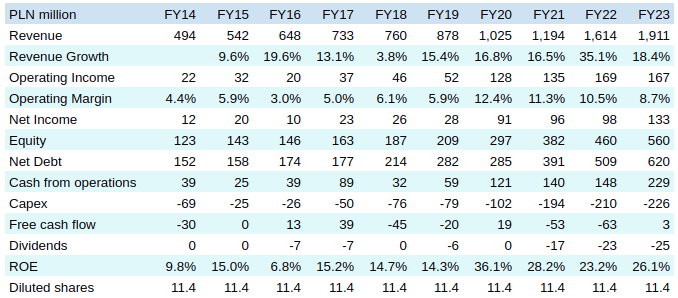

Over the past decade, the Company’s revenue has quadrupled, increasing its market share in kabanos from ca 12% to ca 70%, and with exports increasing from ca 5% of revenue to ca 30% of revenue, proving its ability to enter foreign markets. The Company’s growth has taken place in a mature industry, with pork consumption in Poland remaining relatively stable over that period.

The Company’s operating margin fluctuates over time, notably driven by changes in meat prices. That being said, margins are clearly trending up over time as the Company gains economies of scale.

The Company’s cash from operations has increased strongly as well, and is being mostly reinvested in capex to further increase production capacity. The strong growth was also funded through a PLN45m IPO a decade ago, as well as debt. The Company doesn’t hesitate to lever up to 4x EBITDA - I find that a bit aggressive but the current net leverage is only 1.8x EBITDA and the Company does operate in a defensive industry. It’s noteworthy that all of the Company’s growth has been organic, without any acquisitions. Over the last few years Traczynski has started paying out a dividend as well, although the payout ratio remains quite low.

Management & Ownership

The Company was founded in 1989 by husband and wife Jacek and Elzbieta Tarczynski, who own ca 75% of the capital, directly and indirectly through two entities, EJT Investments Sarl and EJT sp.zo.o. Jacek Tarczynski (62) is still the CEO, and their children also work in the business, with notably Tomasz Tarczynski as head of Sales & Marketing and David Tarczynski as head of development (I take that to mean COO).

There are some related party issues. There are PLN1m loans that were granted to the CEO and a member of the Supervisory Board. And in 2018, EJT sp.zo.o entered into a PLN90m loan to purchase Traczynski shares, as part of a failed attempt to take the company private - it was blocked by minority shareholders who disagreed on the price (the initial offer was at PLN10.5/share, slightly above its lows of the previous year). Tarczynski SA acceded to the loan as a co-borrower and started making repayments, with EJT sp.zo.o then having to pay it back. I don’t like that transaction at all but will treat it as a one-off, as when it was structured the intent was to take the whole company private.

Prospects & Valuation

Management is making large capex investments to increase production capacity, which should lead to further growth, and so far execution has been exemplary. The fact that the Company has a market share of over 70% in Poland may lead one to think that there is limited potential, but Tarczynski has essentially created its own market by expanding supply, and the strong overseas growth is also encouraging.

When I initially started researching the Company and building my stake, it was trading at 6x trailing P/E. But over the last few days the stock price has kept making new highs and multiples went to ca 9x trailing P/E and 9x EV/EBIT before I had the time to press Send on this write-up - I found that particularly frustrating. The stock price went from ridiculously cheap to just cheap. I understand the run-up in price was due to its inclusion in a Polish SMID index, as well as the relatively low liquidity of the shares. Needless to say - the current price is still fine, but buying at 6x trailing P/E would have been even better.

A risk here is that margins are currently at the high end of the historical range and could potentially decline if meat prices increase. I think the shares will do well over the coming years, with increases in volumes and margins expanding driven by economies of scale. But there could be downside if meat prices increase, or just if the P/E multiple declines - Tarczynski has historically traded at an average P/E of 7.5x. At a P/E of 6x I would have made this company one of my core holdings. I didn’t have the time to build a full position and intend to buy more if the share price goes back around PLN100 or below.

As the Company is a small cap with relatively low liquidity, institutional investors will have no interest in it. Average daily volumes are ca 1,700 shares. That’s still sufficient to allow individual investors to build a stake, over a few days if needed.

Conclusion

Tarczynski has an excellent operating track record, with revenue quadrupling over the past decade, net income increasing by 10x, and an average ROE of ca 19%. The Company operates in a defensive and mature industry where it has taken market share through innovation and marketing, qualities not usually associated with meat production. The negatives are the current multiples, which are above historical averages (but still significantly below market averages), as well as the potential for margins to decline if meat prices increase.