Viel & Cie

Financial holding trading at 6x P/E, 1.4x P/B, with ROE of 23% and dividend yield of 3.8%.

Viel & Cie is a financial holding company listed in France with a market cap of ca €704m, which owns stakes in three main businesses:

Compagnie Financiere Tradition, an interdealer broker. This company is listed, with a market cap of CHF1.24bn. Viel owns a ca 71% stake, therefore valued at ca €940m. That business represents ca 95% of Viel’s consolidated revenue.

Bourse Direct, an online stock broker. This company is listed as well, with a current market cap of €281m. Viel owns a ca 81% stake, therefore valued at ca €227m. That represents the remaining ca 5% of Viel’s consolidated revenue.

SwissLife Banque Privee, a private bank in which Viel holds a 40% stake. It is consolidated using the equity method and the stake had a book value of ca €72m at year-end 2023.

Right away we can see that there is a significant holding company discount, with Viel trading for much less than the value of its main stakes.

I’ll now cover the three main businesses in more details.

Compagnie Financiere Tradition

Business: Tradition is an interdealer broker. It acts as middleman, without taking positions itself. In essence, when for example a bank enters into a currency swap with a client, it will want to hedge its own book, and if it can’t offset the transaction internally, will need to go to an external party. Instead of getting in touch with hundreds of other counterparties to negotiate the transaction, it can just contact a middleman: Tradition, or one of its peers. In FY23, Tradition’s revenue by product could be broken down as follows: (i) Currencies & Rates (41%). Consists of interest rate derivatives; money markets; FX forwards; FX options and futures; (ii) Securities and security derivatives (33%). Includes government bonds, corporate bonds, credit derivatives; repurchase agreements; and equities and equity derivatives; (iii) Energy and commodities (23%). Comprises oil, electricity, gas, and metals commodities; and (iv) Retail FX (3%). Gaitame.com, an online retail forex brokerage in Japan.

Financial Overview:

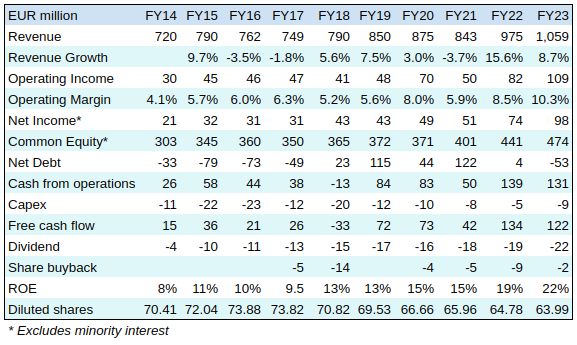

Tradition’s stated operating strategy is to create long term value through organic growth, profitability and cash conversion. Over the last ten years the company has certainly delivered, with solid revenue growth and significant margin expansion, which translated into a nearly quadrupling of the net income and a large increase in free cash flow generation.

The company’s financial strategy is conservative and shareholder friendly. Management is focused on a sound balance sheet, visible at the net cash position as well as the high and increasing equity base. And Tradition has a policy of distributing a consistent dividend, complemented with a share buyback program; the dividend and dividend per share have significantly increased over time, although the diluted share count did increase slightly as well, the only negative element so far.

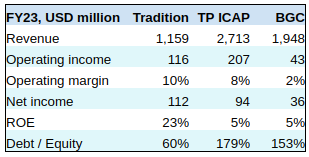

Peer Group: Tradition is one of the top three global interdealer brokers. It effectively operates in an oligopoly, with TP ICAP and BGC. If we do a high level peer comparison we can see that Tradition is the smallest of the three, however it is better run, with higher operating margin, higher net income, significantly higher return on equity and lower debt.

Bourse Direct

Business: Bourse Direct provides Internet stock brokerage services in France. This company is relatively small, with ca 333k client accounts, and competes with much larger peers.

Financial Overview:

Bourse Direct performed quite well over the past decade, with solid revenue growth over the past decade. Operating income has been particularly strong in recent years driven by increased trading and higher interest rates, which has allowed the company to start paying dividends.

SwissLife Banque Privee

SwissLife operates mostly in private banking, with €7.4bn in assets under custody at the end of 2023. There is less available information on this company but it is also performing well, with €46.8m in net income in 2023 (Viel share: €18.7m), compared to €24.8m in 2022 (Viel share: €9.9m), and for a book value of €72.3m.

Viel & Cie

Now that we have looked at the main stakes, let’s review Viel’s consolidated accounts:

Unsurprisingly, Viel’s accounts are very similar to those of Tradition, its main stake. The shareholder remuneration policy is impeccable, with solid dividend payments and share repurchases leading to a decreasing share count. Viel also keeps slowly increasing its ownership of Tradition and BourseDirect.

Viel just released 1H24 results, which were once again stellar: 9.7% revenue increase at constant exchange rates to €597m; 15% increase in operating income; 31.4% increase in net income to €65.4m. Management also mentioned that its businesses continued to perform well in the months of July and August, and with good prospects for the coming months. The Viel stock price jumped by over 8% on the news, but the shares still trade at only 6x earnings.

Management & Ownership

The longstanding CEO and main shareholder is Patrick Combes, with a 69.88% stake. He reportedly took over Viel in 1979, which back then was a small and old Parisian broker with only three employees. The small brokerage was able to grow at a fast pace thanks to deregulation and strong business acumen. Mr Combes then realized he needed global scale as well as a better range of products, and managed to take control of Tradition in 1996, a much bigger operation that had fallen on hard times and was successfully turned around. He created subsidiary Bourse Direct in 1999 to take advantage of the internet; Mr Combes purchased a 40% stake in SwissLife in 2007.

Conclusion

Viel owns stakes in three solid businesses that are all performing well, with a solid track record evidenced by a high and increasing ROE, and good prospects.

Holding company discounts are usually warranted by a lack of control over underlying assets; management costs and inefficiencies; or corporate governance concerns. Here, Viel controls Tradition and Bourse Direct, in which it keeps increasing its ownership, and corporate governance is exemplary, noting the dividend policy and decreasing share count. I would not expect the holding company discount to disappear anytime soon as it has been there for decades. Nevertheless, the current share price of 6x P/E for a collection of growing businesses coming with a net cash position is obviously cheap, and as Viel is repurchasing its own shares, fine with me if the share price remains undervalued. Part of the reason for the cheapness may also be the lack of liquidity: the average daily volume is ca 6.5k and the free float amounts to ca €211m in total. This is too small for institutional investors, which as an individual investor I see as another advantage - there is no competition for the shares.

I like to own businesses that are cheap; generate cash; and return that cash to shareholders through dividends and share repurchases. Viel ticks all the boxes.